How will inflation impact future returns for the Nasdaq 100 index? Is the Nasdaq 100 index a good investment as of today?

And how will FAANG stocks ($AMZN, $AAPL, $MSFT, $GOOGL) impact QQQ?

TLDR: Inflation is probably going to stick around at least (3-4%) for the next 3-5 years. It is going to be a headwind for stock prices and drive down valuations. 46% of Nasdaq 100 is dominated by top 6 companies, who have grown humongous and are on an average expensive on a P/E ratio. Also, there is less likelihood that a new set of firms will emerge to replace FAANG and achieve trillion dollar valuations for a few years. Thus, if you believe that the top six firms are too big to grow as fast as they have and also believe that valuation matters, investing in the Nasdaq 100 may not get you impressive returns in the next 10 years. The next article will contain some alternatives to Nasdaq 100 for the curious investor.

Background

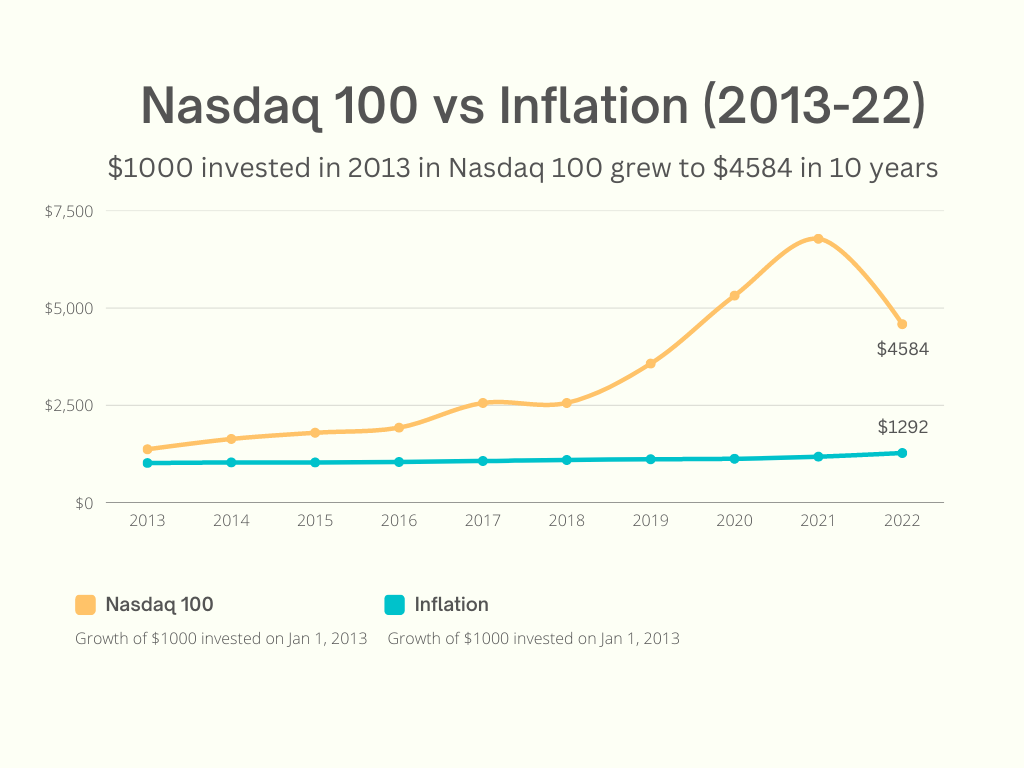

To start, let us take a look at the Nasdaq 100 returns and the corresponding annual inflation. If you invested $1000 in Nasdaq 100 in 2013, you had $4584 at end of 2022, vs just $1292 if you had kept pace with inflation.

What were the reasons for this stupendous growth?

Explosive Growth in trends of Cloud, Social Media, Digital Advertising, E-Commerce

Last ten years were helped by the explosive growth in trends of Cloud (Amazon, Microsoft), e-commerce (Amazon), Social Media (Meta) and Digital Advertising (Google, Meta). All these trends and the resulting explosive growth was enabled by the powerful network effects of the Internet, which first started taking shape in the 2000s. The Internet and the resulting trends were a paradigm shift similar to the advent of personal computers in the 1980s, and may be tough to repeat.

Low interest rates enabled investors, companies to invest in future (and profitless) growth

Low interest rates on cash and bonds reduces the rate of return that investors can earn from such assets, thus forcing them to invest their money in riskier assets like stocks, hoping for a better return. In addition, tech companies were able to borrow cheap money to invest in projects with little or no chance of profits - thus helping accelerate their revenue growth. Expectations for better returns and profitless revenue growth helped drive stock prices up.

One can see this trend in the rise in Venture Capital funding - according to Pitchbook; VC funding in 2021 increased to $329.9B vs $27.8B in 2009, a 10x increase. By nature, Venture Capital investments are riskier in comparison to stocks or bonds.

What (is most probable) about the future trajectory of inflation?

When we invest our money, the future is inherently unknowable, but we need to make a best guess of what happens next. Howard Marks, the billionaire investor, came up with a new memo - Sea Change - he makes a convincing point that we are in the midst of a sea change, the only third one he has seen since in the last fifty three years of his investing career.

He says: “ I believe that the base interest rate over the next several years is more likely to average 2-4% (i.e., not far from where it is now) than 0-2%. “

One may ask - Why will interest rates still remain high in comparison to earlier cycles when the Fed was able to cut the interest rates to zero?

The Fed’s charter is to keep inflation near or below 2%, and if inflation creeps up beyond their target rate, they need to increase the Fed's fund rate close to the prevailing inflation rate to bring down inflation. The following factors will prevent inflation from reaching a range of 0-2% again in the next 5-10 years.

Reversal of Globalization: The earlier policy of zero interest rates was enabled by cheap overseas markets which kept inflationary pressures on prices of everyday goods and services in check. With the reversal of globalization (due to geopolitical tensions with Russia and China), companies will re-shore thus raising prices for their goods.

Trend of Rise in Wages of Service Economy Workers: Labor market data indicates that, since the onset of COVID, U.S. service economy workers have demanded, and received, wage increases at faster rate than the previous 30 years -- thereby pushing inflation up.

Finally, when trends start, they often last for more than a few years. The interest rates declined from ~20% in 1981 to around 0% in 2022 - a period of 40 years. Thus, if the trend is turning, it is highly likely that we will have moderately high interest rates (3%-4%) for a few years.

How does inflation impact our expectations of stock prices?

If we do believe inflation remains higher for longer - even 3-4% - then we need to readjust our expectations from the stock market. Let us take a brief segue to understand how stocks can be valued in a manner similar to bonds. The price earnings (P/E) (a common way of valuing stocks) ratio of 20 implies that you are paying a price that is equal to the earnings that this company will generate in the next 20 years - it implies an earnings yield of 1/20 = 5%.

Thus if interest rates of US treasury bills yield 3-4%, an investor in stocks will expect a higher return as stocks are riskier vs treasury bills - and thus will expect that the earnings yield of stocks in the range of 5-7% (a range of P/E of 15 to 20). Even after recent declines, the Shiller Cyclically Adjusted PE (CAPE) ratio is 27.8 vs a long term average of 17. Robert Shiller, Nobel laureate, created the CAPE ratio which adjusts for a cycle of earnings for 10 years, to avoid the impact of yearly fluctuations of earnings.

How will Inflation impact returns from Nasdaq 100 for the next 10 years?

Half the Nasdaq 100 index is dominated by six big companies!

If we evaluate the Nasdaq 100 index, it is dominated by big companies - 46% of the index is dominated by the big six (Apple, Alphabet, Amazon, Microsoft, Nvidia, Tesla and Meta) companies, which on average are expensive on P/E ratio.

An aside: these six companies constitute a big portion ( 19%) of the S&P 500 index too.

The chance that Nasdaq 100 produces an impressive return over the next 10 years seems less likely because almost half the index is constrained by expensive companies.

The top six companies in Nasdaq 100 are very big

The impressive returns that you saw in Nasdaq were driven by companies like Google that grew from $235B Market Cap in 2009 to $1.1T in 2022, and Apple grew from $80B in 2009 to $2.1T in 2022. Given their huge size, regulatory/ antitrust pressures, it's hard to imagine that these companies will continue their impressive growth rates.

The top six companies are expensive on a P/E ratio and their future growth may already be accounted for in their current stock prices. A good example is Cisco, at the height of the previous dot com bubble - the price/earnings ratio of the company was 196 in the year March 2000 - and even though revenues of Cisco has increased from $19B in 2000 to $52B in 2022, its price/earnings ratio has decreased from 196 to 16. Thus, ultimately, the valuation ratio one pays has at least some determining factor in one’s returns.

It is highly probable that we hit peak valuation in Nov 2021: In Nov 2021, 5 US companies (Apple, Amazon, Alphabet, Tesla and Microsoft) hit a trillion dollar valuation or higher - this was driven by low interest rates, and extraordinary technology spending driven by pandemic. One can argue that another new trend may emerge - and a new iteration of FAANG companies emerge - but trends take time and it is improbable that we have another new set of trillion dollar companies until 2030.

Thus, If one wishes to invest in technology, there may be other better opportunities vs investing in Nasdaq 100 (QQQ). Ideas for where opportunities may lie will be outlined in the next write-up in this series.

Note: None of this is investment advice, and prediction is often futile.

“The financial markets generally are unpredictable. So that one has to have different scenarios... The idea that you can actually predict what's going to happen contradicts my way of looking at the market.” ~ George Soros

Disclaimer:

This blog is solely for informational purposes and is not intended to be a solicitation to buy or sell any particular security. We suggest you check with a broker or financial advisor before making any investing decisions.

The author is affiliated with Tilden Path Capital, registered as a Registered Investment Advisor in California.

Past performance is no guarantee of future returns.

All investing involves risk and possible loss of principal.

In our analysis, we use third-party resources we believe to be reliable, but cannot guarantee the accuracy of such information. We believe the information we provide is accurate as of the date furnished, but we do not revisit past material to update it.